Brad Ferris

I believe I had my first Coca-Cola in either 1935 or 1936. Of a certainty, it was in 1936 that I started buying Cokes at the rate of six for 25 cents from Buffett & Son, the family grocery store, to sell around the neighborhood for 5 cents each. In this excursion into high-margin retailing, I duly observed the extraordinary consumer attractiveness and commercial possibilities of the product. I continued to note these qualities for the next 52 years as Coke blanketed the world. During this period, however, I carefully avoided buying even a single share, instead allocating major portions of my net worth to street railway companies, windmill manufacturers, anthracite producers, textile businesses, trading-stamp issuers, and the like. (If you think I'm making this up, I can supply the names.) Only in the summer of 1988 did my brain finally establish contact with my eyes.” -- Warren Buffett (1989).

There are a great number of investors who quote Warren Buffett, follow his investment activities and attempt to walk in his footsteps in the hope of achieving success. I was taught some time ago that investors all too often neglect stocks with a reasonable valuation and dominant fundamentals in favour of buying companies with discounted valuations and less dominant fundamentals. I’ve learnt this by taking the time to study the best, the brightest and the most fallible of investors in my pursuit of understanding their behaviour, motivation and investing process.

What Buffett is talking about in reference to his eventual investment in Coca-Cola (KO) after staring it in the face for over half a century is the concept of Enduring Value. The label of Enduring Value is often easy to recognize after a corporation's decades of solid performance and successful global achievements, but difficult to identify in the early phases of a company’s history.

I was reminded of this quote by Buffett the very first time I read through the 2004 Annual Report of Manulife Financial (MFC). At the time I was just beginning my mentorship under a great investor and looking to apply the early lessons I had crafted on stock analysis. Beyond the numbers, financial statements and discussions on investments stood a business that was superbly managed and growing. Manulife had only been a publicly traded corporation since 1999 but almost immediately I gained insight into not just where the company had been but where it was going. The presentation of the company was clear, the expectations from management were evident, a strong financial base sustained and a wonderful track record of accretive acquisitions implemented effectively.

The Manufacturers Life Insurance Company (Manulife) dates back to 1887 when Sir John A. Macdonald, Canada’s first prime minister, was elected president of the company. Manufacturers Life was then one of the first companies to offer women life insurance on the same basis as men – a highly controversial and innovative decision at that time.

In 1893 Manulife sold its first insurance policy outside of Canada beginning what would later become a tradition of expanding operations internationally. By 1897 Manulife had expanded into Asia and from 1900-1950 had operations to the Philippines, Indonesia, the United States and United Kingdom. By 1980 Manulife was operating joint ventures in Singapore, acquiring US & Canadian insurance operations, and in 1996 opened China’s first joint venture life insurance company. The company currently has global operations in Canada, the United States, Asia & Japan, selling a diverse portfolio of insurance and investment products.

In 1994, Manulife announced the appointment of Dominic D'Alessandro to Chief Executive Officer and who later led Manulife on its acquisition path that in 2004 purchased Boston based John Hancock Financial Services for $10.4B.

I have always believed that great business is conducted by great people and that integrity, values and discipline are the hallmark of any great leader. Manulife not only has had a great leader, but a collection of great people running operations of their business around the world. In a top-down approach the values of the company are prominently demonstrated by its leaders. Through his executive track record, charity and attitudes towards the business he expects his company to conduct, Dominic D’Alessandro will be a substantial loss for the company when he steps down in May of 2009. His replacement will be Donald Guloien, currently Chief Investment Officer of Manulife. Donald has been employed with Manulife since 1981 and was responsible for integrating the investment operations of Manulife with John Hancock during its 2004 acquisition of the company.

One of the first things that I always notice whenever I read the annual reports on Manulife is the clear and concise definition of corporate culture. The company’s values are described publicly through the acronym PRIDE which stands for Professionalism, Real value to our customers, Integrity, Demonstrated financial strength and Employer of choice.

Investors should realize that values, corporate culture or a mission statement can mean little if not executed or demonstrated in a top-down approach. Management should demonstrate not on a “do as I say” but a “do as I do” modelling of how a company conducts itself both internally and externally. In any public statement, interview or speech provided by the senior management of Manulife is the clear expectation that this is how the company expects to do business now and moving forward.

During the past two years there has been an intent focus on credit quality, available corporate liquidity and risk. Risk management has been the new corporate buzz word on Wall Street and Bay Street with corporations and business schools making public acknowledgements that risk management is a top priority of their corporate culture or curriculum. As an investor and businessman I know there is a significant difference between saying and doing and when management says one thing I expect them to walk instep with their public and private commitments.

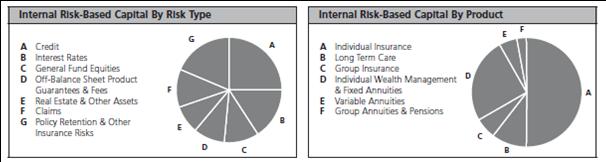

Manulife has a strict risk management culture that included oversight governance from a Product Oversight Committee, Credit Committee & Global Asset Liability Committee. Since going public as a corporation, Manulife has clearly presented to investors the risk management policy, expectations, identification & monitoring, measurement, controls and mitigation activities they have in place. In their 2007 Annual Report they clearly define their strategic risk, market risk, foreign currency risk, credit risk, insurance risk, liquidity risk, operational risk, derivatives risk, interest rate risk and risk from variable products & managed assets.

If I can add a perspective:

There are ten pages or 8% of the 2007 annual report devoted to strictly conveying risk that the company is exposed to in its various operations in detail for shareholders. These aren’t hidden in the notes of financial statements or written in fine print as legal disclaimers at the end of the report. In each annual report Manulife commits an entire section to the explanation of risk and this isn’t a recent event in light of the credit crisis. As a percentage of the annual report risk management was:

- 8% in 2006

- 6% in 2005

- 7% in 2004

- 11% in 2003

As you go through those reports Manulife’s risk profile has changed little over that period.

Financial strength of the company and credit ratings, in light of recent events, remain strong.

One difficulty in evaluating any insurance company is gaining an appropriate assessment of its bond and investment portfolios. With the Lehman Brothers and large financial failures in 2007 and throughout 2008 we’ve seen many companies take large write-downs on losses through direct or indirect credit exposure. Manulife stated in September that less than 1% of its $164B in assets has exposure to Lehman Brothers, AIG or Washington Mutual and that its par value investments in each respectively was $395M, $374M and $41M.

The company has stated that $96B of its bond portfolio is rated at investment grade or better (BBB or higher). In my research the lowest component of its bond and private placements has a rating of 80% investment grade and comprises only 4% of the portfolio in the category of basic materials. 27% of the portfolio is Government and agency bonds with 22% in financials.

Its investment division holds 45% bonds, 7% of stock, 16% mortgages and 13% private placements. Mortgages are comprised of 55% Canadian and 45% US with 74% of total mortgages as commercial and 21% of the total portfolio as government insured. The remainder of the non-commercial mortgages are Canadian residential and agricultural.

Since 45% of Manulife’s investment portfolio is comprised of bonds, some future losses are likely to materialize. Greater transparency of the bond portfolio would be helpful in any assessment, but likely due to the size and scale of the portfolio very few investors would have the time to perform a comparative risk assessment based on any number of factors.

Segregated funds have been a major concern of the equity markets in recent weeks and put Manulife and other insurers in the spot light. Segregated fund products in recent years have been very attractive to insurance companies and aggressively sold to investors seeking capital preservation of their investments with the potential benefit of upside as markets appreciate. As equity markets have declined significantly in recent months, questions have been raised about these products and whether additional capital needs to be raised in order for companies to meet these longer-term obligations.

In my situational analysis, one significant internal threat for my investments in insurance companies has been the increased affinity for these products. While they offer lucrative fees and an incentive from the issuing company’s perspective, the explosive growth of these products has been concerning and likely something that will be appropriately managed in future years.

One benefit is that although segregated products have been sold by Manulife in all their major markets, many of these products do not require repayment for another 7 to 30 years, and the potential costs of these products are within the stated resources of the company. Manulife continues to operate above any regulatory minimum for its capital ratios and has not yet taken significant losses attributed to these products.

So now I have to try and answer some difficult questions:

- Do I trust management?

- Do I approve of the plan for CEO succession?

- Are the business model and business operations sustainable?

- Will the company continue to be profitable?

- Is there an element of Enduring Value?

- Have any competitive disadvantages emerged?

- Do strong fundamentals of the business, markets and customers remain?

- What am I willing to pay for the risks that have been highlighted?

At this point in my analysis I want to go back to the numbers to see how the company has performed by putting its business model into perspective. I know from following the company that earnings have not benefited or been inflated from the business being over leveraged as we saw in recent years with many large financial institutions. The company does not have material exposure to derivatives or subprime mortgages and the company has never been investigated or performed questionable accounting.

Going back to 1995 I have the following historical data on the company:

- ROE: 14.8%

- Div Yield: 1.75%

- Payout: 25.9%

- P/E: 15.4x

- P/B: 2.32

- Div Growth: 22.3%

- BV Growth: 12.2%

Current Data:

- Dividend: $1.04

- BVPS: $15.80

- EPS (ttm): $2.70

- Yield: 4.20%

- Payout: 38.5%

- P/B: 1.58x

If I apply my dividend discount model to determine a FMV for Manulife as previously shown I have a few issues first to resolve.

(For investors looking to gain insight into my rationale of the next section please review parts III and IV of my fundamental analysis series).

As a value investor I need to recognize a few potential outcomes of any investment in this environment. I know that earnings, over the interim, are likely to either compress due to market weakness or stagnate under continued growth pressures. There’s also potential that an investment will experience dilution from issuance of additional common shares in the event the company needs to raise capital (assume 10% dilution). Despite my confidence in strong operating fundamentals of the company I need to provide a realistic valuation to best protect myself from risk.

I have a few options:

- I can stay consistent with my traditional valuation method

- Increase my discount rate beyond 25% to 50% to account for the greater equity risk

- Discount my expectations of full EPS for the full year 2009

- Take into consideration a worst case scenario of a 50% drop in EPS & 40% cut to the dividend

Growth Rate

= [Historical ROE / Current P/B] + Historical BV Growth)

As you can see this gives me a wide range of potential valuations depending on how risky I view the investment to be. When I summarize my situational analysis, including all potential outcomes for risk, I’m confident in selecting #3 as the most appropriate valuation at this time disclosing to readers that #1 is my original FMV through which I bought the shares in May of 2007.

My reasoning for choosing #3:

The company has a targeted dividend payout of 25-35% and the payout currently sits at 38.5% which is only slightly above the historical high side for the company. The dividend in my view is safe as the company’s revenues and earnings are diversified in a number of markets and financial products. The company has adequate financial resources to sustain the dividend, and earnings, as of right now, have not shown any substantial weakness that would indicate otherwise. Capital ratios for the company remain above regulatory thresholds and investments are diversified by risk in a number of asset classes and groups.

I do expect earnings to drop slightly as write-downs and loss provisions are taken to better position the company for an eventual acquisition. What I don’t anticipate is a drop of greater than 20% to full EPS for 2009 from their current level.

At current prices Manulife is likely undervalued by approximately 15% or more. At its recent 52-week low of under $22 my analysis indicates that the market perceived a drop of 50% in EPS for 2009 and a dividend cut of 40% or was looking for an adequate margin of safety nearing 50%. While I cannot rule out the possibility of a serious earnings decline or dividend cut, my experience, analysis and confidence in management indicate to me that the outcome for a dividend cut and sustained drop in earnings is remote.

If the company were to issue common shares to the effect of a 10% dilution, I would take the opportunity to add to my position as I view that move as prudent given the current market environment and potential for accretive acquisitions. The company is a long-term investment for my portfolio and has been wonderfully managed before this crisis to position itself in a conservative financial position and I don’t see signs of that changing now. Management was not motivated to take extreme risks in their financial products and the investment portfolio is well diversified in terms of risk. While I can’t promise that losses from certain investments won’t have an impact on earnings I do have confidence in the ability of current management to position Manulife for growth moving forward.

Disclosure: I own common shares in MFC.

Ref:http://seekingalpha.com

No comments:

Post a Comment